The UK retail sector in April 2025 presented a blend of steady recovery and ongoing structural challenges across various segments. According to the Office for National Statistics (ONS), independent retailers showed positive momentum in several categories compared to April 2024, reflecting a rebound in consumer confidence, seasonal factors, and evolving market trends. This report examines the performance of key retail sectors, exploring potential reasons behind the changes and what they reveal about the wider retail landscape.

Independent Clothing Stores: Recovery Slows but Remains Positive

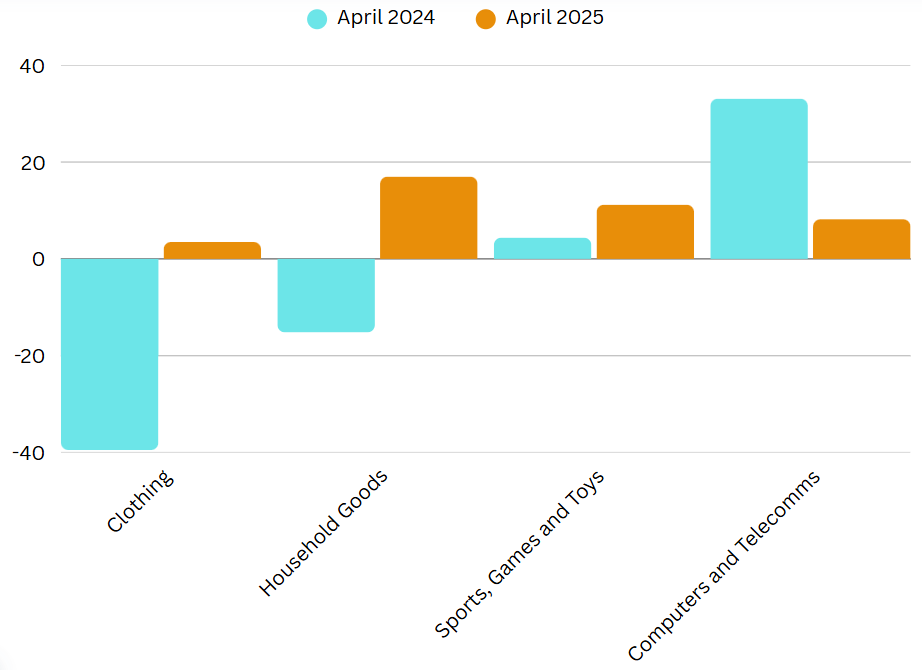

Independent clothing stores reported a 3.5% increase in sales in April 2025, building on the stronger 15.4% growth seen in March. This marks a sharp contrast to April 2024, when sales fell by 39.5%. According to The Guardian, the significant drop in 2024 was largely due to the ongoing cost of living crisis, which led many consumers to reduce discretionary spending on non-essential items like clothing. Inflationary pressures and energy costs continued to squeeze household budgets throughout 2024, contributing to widespread store closures in the sector.

By April 2025, stabilising inflation and improving wage growth, as noted by the Bank of England in its March 2025 Monetary Policy Report, provided some breathing room for consumers. Additionally, the Met Office reported a warmer-than-average April, which likely encouraged shoppers to refresh their wardrobes for spring. However, while the monthly increase is positive, the slower growth compared to March suggests that recovery in the clothing sector remains fragile, with lingering competition from fast fashion giants and online marketplaces.

Independent Household Goods Stores: A Strong Surge

Independent household goods stores saw a 17% increase in sales in April 2025, following a 13.6% gain in March. This represents a significant turnaround from April 2024, when sales dropped by 15.2%. According to Reuters, the surge in household goods sales is partly driven by consumers investing in home improvement projects, motivated by stabilising mortgage rates and a focus on enhancing living spaces.

Furthermore, the easing of energy bills, as reported by the BBC, has freed up some household budgets, allowing more discretionary spending on home-related products. Promotional offers and extended financing options introduced by many independent retailers in this sector have also helped attract cost-conscious shoppers looking for value and quality.

Sports Equipment, Games, and Toys: Continued Growth in an Active Market

The sports equipment, games, and toys sector recorded an 11.2% increase in April 2025, following a 15.1% rise in March. This compares favourably to April 2024, which saw a modest 4.4% gain. According to Mintel’s 2024 UK Health and Fitness Market Report, consumers continue to prioritise health, wellness, and outdoor activities, driving demand for sports equipment and active lifestyle products.

The timing of school holidays in April, alongside favourable weather, likely contributed to stronger sales in outdoor games and family-oriented recreational products. Additionally, the enduring popularity of home-based gaming, fuelled by new console releases and subscription services, has helped sustain growth in this sector.

Computers and Telecom Equipment: Growth Slows as Market Matures

Sales in the computers and telecom equipment sector rose by 8.2% in April 2025, following a 16.5% increase in March. However, this growth is more subdued compared to the 33.1% surge recorded in April 2024. According to the Financial Times, the exceptional growth in 2024 was driven by pent up demand following pandemic related digital transformation and remote working trends.

By 2025, much of that demand has been met, leading to a natural cooling-off period. Market saturation, fewer major product launches, and cautious business investments have also tempered growth. However, as noted by Ofcom in its 2025 Telecoms Update, there remains a steady underlying demand for 5G connectivity and small business digital infrastructure upgrades, supporting moderate growth in the sector.

Conclusion

April 2025 reflects a retail sector in cautious recovery, with positive trends across independent clothing, household goods, and recreational categories. While growth has moderated compared to the stronger gains of March, year on year comparisons show a marked improvement from the difficult trading conditions of 2024. Independent retailers who continue to innovate, focus on value, and adapt to shifting consumer behaviours are well-placed to navigate the evolving market landscape. The outlook for the coming months will depend on the broader economic environment, consumer confidence, and the ability of businesses to remain agile and customer focused.

The UK’s independent retail sector in March 2025 delivered encouraging signs of recovery, with strong performances in key categories like clothing, household goods, and recreational products. While some growth can be attributed to favourable weather conditions, broader consumer trends, market adjustments, and macroeconomic pressures also shaped results. This report, grounded in data from the Office for National Statistics (ONS), explores the comparative performance of March 2025 and March 2024 across four independent retail categories and investigates the potential reasons behind these shifts.

Independent Clothing Stores: From Decline to Growth

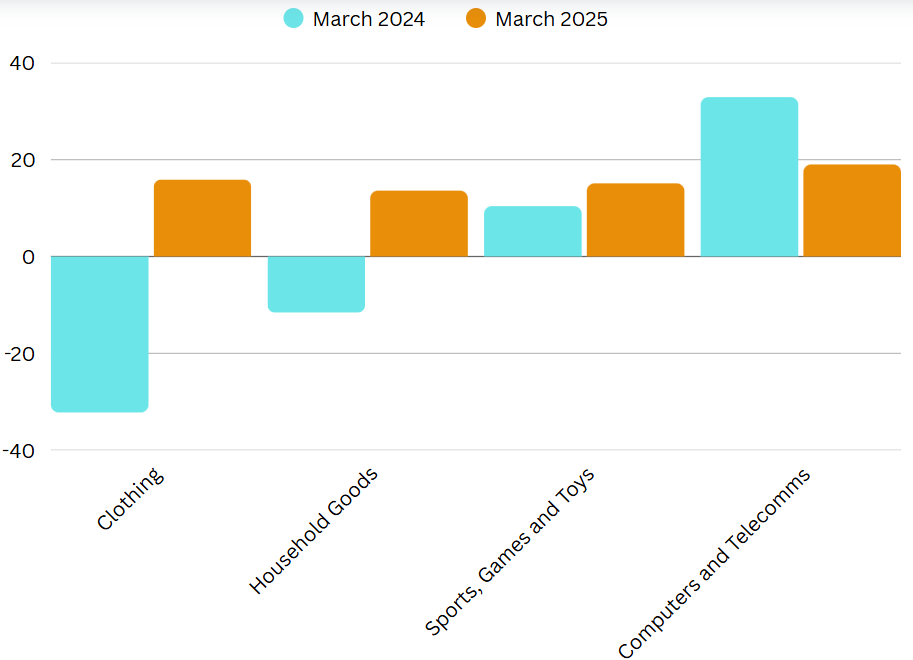

Independent clothing stores saw a 15.9 percent increase in March 2025, their first monthly rise since before 2024. This marks a sharp turnaround from the 32.2 percent drop recorded in March 2024 and is a significant improvement from February 2025’s 10.4 percent decline. Despite this monthly rebound, sales for the first quarter of 2025 remain down by 3.3 percent compared to quarter one 2024, which itself saw a steep decline of 30.9 percent.

According to The Independent, the deep fall in 2024 was largely driven by the cost of living crisis and inflationary pressures that eroded household purchasing power, pushing nonessential spending including clothing down the priority list. By March 2025, inflation had eased slightly and real wages improved marginally, as noted in the Bank of England’s March 2025 Monetary Policy Report, helping consumers regain confidence and spend modestly on discretionary items.

Warmer than average weather during March also played a part. According to the Met Office, March 2025 was one of the sunniest on record. This seasonal shift likely prompted early spring wardrobe updates, contributing to the positive retail performance.

Independent Household Goods Stores: Momentum from Refurbishment and Recovery

Sales at independent household goods stores increased by 13.6 percent in March 2025, building on February’s 12.2 percent gain and marking a reversal from the 11.6 percent drop seen in March 2024. Quarter one of 2025 showed a 7.5 percent increase overall, compared to a 7.9 percent decline during the same quarter in 2024.

This growth reflects renewed interest in domestic improvement. According to a 2025 report by Kingfisher, the parent company of B&Q, demand for home and garden products rose sharply in early spring as consumers engaged in seasonal DIY. Additionally, with mortgage approvals recovering and house prices stabilising, more homeowners appeared willing to reinvest in their living spaces.

Reuters has also pointed out that competitive pricing and discount led promotions have helped drive demand in this sector. Many independent retailers took cues from larger chains by offering bundled deals or time limited discounts to clear seasonal inventory, encouraging consumer uptake in March.

Sports Equipment, Games, and Toys: Healthy Lifestyles Drive Demand

The sports equipment, games, and toys sector experienced a 15.1 percent rise in March 2025, continuing from February’s 17.6 percent increase. This builds on March 2024’s 10.4 percent growth and contributes to a 14.7 percent gain for the entire first quarter of 2025, up from 9.1 percent in quarter one 2024.

According to a consumer trend report from Mintel, increased health awareness and at home fitness trends that grew during the pandemic have now become embedded consumer habits. These patterns are particularly strong in the independent retail space, where niche and high quality fitness equipment, outdoor games, and eco conscious toys continue to attract engaged customers.

Moreover, March’s mild and sunny weather conditions made outdoor activities more appealing, driving up purchases of equipment related to running, cycling, and gardening. The Sports and Outdoor Equipment Retail Association also noted that independent retailers have benefited from customer preference for personalised service and community based retail, especially as larger chains consolidate their physical footprint.

Computers and Telecom Equipment: Growth Slows in a Saturated Market

Computers and telecom equipment saw a 19 percent increase in March 2025, following a 5.2 percent gain in February. However, the growth is markedly slower compared to March 2024, when sales rose by 32.9 percent. For the first quarter of 2025, the sector posted a 7.2 percent increase, well below the 28.3 percent gain reported in quarter one 2024.

According to the Financial Times, much of the explosive growth seen in early 2024 was driven by pent up demand following the post pandemic digital transformation of homes and small businesses. By 2025, the market has matured, and many consumers have delayed upgrading devices due to cost of living concerns and the absence of new product launches from major tech brands in the first quarter.

That said, demand remains stable for telecom infrastructure and networking hardware. As noted by Ofcom’s 2025 Telecoms Update, small business adoption of fibre broadband and 5G compatible equipment continues to rise steadily, especially in rural and semi urban markets, segments often served by independent retailers.

Conclusion

March 2025 marked a more optimistic phase for many independent retailers, with clothing, household goods, and recreational categories all posting strong results. Improved weather, cautious economic recovery, and shifting consumer priorities contributed to these gains. However, challenges remain, particularly in tech, where the growth curve has flattened due to market saturation.

As seen throughout this report, resilience and adaptability remain central to the success of the UK’s independent retail landscape. Retailers who continue to respond to evolving consumer expectations, embrace digital infrastructure, and maintain a strong community presence are well positioned to capitalise on emerging opportunities in the months ahead.

The UK retail sector in February 2025 exhibited a blend of recovery and ongoing challenges across various segments. According to the Office for National Statistics (ONS), certain sectors demonstrated significant growth compared to February 2024, while others continued to face declines. The driving forces behind these changes include shifting consumer behaviour, economic conditions, and evolving industry trends. This report delves into these trends, exploring potential reasons behind the observed changes and what they indicate for the broader retail landscape.

Independent Clothing Stores: Moderated Decline

In February 2025, independent clothing stores experienced a 10.4% decrease in sales, an improvement from the 32.3% decline recorded in February 2024. Also an improvement from January 2025 where there was a decline of 16.8%. According to The Independent, the sharp drop in 2024 was largely due to the cost-of-living crisis, which significantly reduced consumer spending power across the UK. With inflation peaking in late 2023 and energy bills placing strain on household budgets, non-essential purchases such as clothing were among the first to be cut back. By early 2025, while economic pressures remained, stabilising inflation and stronger wage growth helped ease the squeeze slightly, leading to a more modest decline in clothing sales. Nonetheless, the sector continues to grapple with long-term shifts towards online shopping and discount-driven buying habits.

Additionally, persistent inflation and higher living costs may have led consumers to prioritise essential spending over discretionary fashion purchases. The slow recovery in independent clothing retail underscores the sector’s need for adaptation, possibly through digital transformation, loyalty schemes, and omnichannel strategies to remain competitive.

Independent Household Goods Stores: First Uptick Since 2023

Independent household goods stores reported a 12.2% increase in sales in February 2025, marking the first growth since November 2023. This contrasts with a 4.4% decline in February 2024 and a 1.2% decrease in January 2025. According to Reuters, this resurgence is attributed to widespread discounting and strong consumer demand for household items, as retailers offered promotions to stimulate sales.

Additionally, the rising popularity of home improvement projects, driven by hybrid work arrangements and a desire for upgraded living spaces, has played a role in this turnaround. With mortgage rates stabilising, more homeowners may have been willing to invest in home renovations, further driving demand for household goods. The long-term sustainability of this recovery will depend on economic stability and consumer confidence.

Sports Equipment, Games, and Toys: Sustained Growth

The sports equipment, games, and toys sector continued its upward trajectory with an 18.5% sales increase in February 2025, building upon a 11.2% rise in January 2025 and a 7.5% rise in February 2024. According to the ONS, this consistent growth reflects a sustained consumer interest in health, fitness, and home-based entertainment. The fitness industry has continued to benefit from increased awareness of health and well-being, particularly as people seek long-term alternatives to gym memberships, such as home exercise equipment.

Additionally, gaming has remained a strong driver in this category, with new console releases, esports popularity, and subscription gaming services fueling consumer demand. The sector’s resilience suggests that consumers are still willing to spend on recreational products, even in uncertain economic times.

Computers and Telecom Equipment: Rebounding Sales

Sales in the computers and telecom equipment sector rose by 8.3% in February 2025, recovering from a 2.1% decline in January 2025. However, this growth is modest compared to the 29.7% increase seen in February 2024. According to the Financial Times, factors such as market saturation, slowed business investments, and economic uncertainties may have tempered the rapid expansion witnessed in the previous year. The demand for high-end consumer technology has cooled slightly as many households and businesses upgraded their devices during the peak remote work period of 2020-2023.

However, recent innovations in AI-driven computing, 5G connectivity, and sustainability-focused tech solutions have spurred renewed interest in the sector. Another factor influencing this modest recovery is the government’s push for digital infrastructure investments, which has encouraged businesses to upgrade their telecom systems. While the sector remains strong, its growth trajectory suggests a shift from rapid expansion to steady, innovation-driven demand.

Looking Ahead

The recent implementation of tariffs by U.S. President Donald Trump has introduced significant shifts in global trade dynamics, with notable consequences for the UK economy and its retail sector. Effective from April 5, 2025, the U.S. imposed a 10% tariff on imports from numerous countries (including the UK), escalating to 20% on goods from the European Union and up to 54% on Chinese products.

While Trump’s new tariffs pose clear challenges for the UK, they might also offer some unexpected opportunities. Countries hit hardest by the U.S. tariffs like China and EU nations could look to reroute their goods through the UK to avoid the steep costs. If the UK can negotiate favourable trade deals, it could become a key player in moving goods around the globe, which would give a boost to areas like shipping, logistics, and distribution.

For UK retailers, though, the shake up means rethinking where their stock comes from and how much it costs. They may need to find new suppliers, spread out their risk, and get smarter about pricing to keep customers onside. While the situation brings short term uncertainty, it could open the door for UK businesses to reposition themselves in a changing global market if they move quickly and strategically.

Conclusion

The retail landscape in February 2025 reflects a complex interplay of recovery and ongoing challenges. While sectors like independent household goods and sports equipment have shown notable growth, independent clothing stores continue to face declines, albeit at a reduced rate. The computers and telecom equipment sector’s modest rebound suggests a cautious optimism tempered by market realities. Understanding these dynamics is crucial for retailers, policymakers, and investors, as it highlights the importance of adaptability in a rapidly evolving market. Future growth will depend on economic stability, consumer confidence, and the ability of businesses to leverage digital transformation and emerging trends to their advantage.

In January 2025, the UK retail sector exhibited varied performance across different categories. Independent clothing stores continued their downward trend, albeit with a less pronounced decline than in January 2024. Independent household goods stores showed signs of recovery, outperforming their January 2024 figures. Conversely, independent food stores experienced a dip compared to the previous year, following a strong 2024. The sports equipment, games, and toys sector saw significant growth, building on an already successful year. Meanwhile, the computers and telecom equipment sector maintained positive performance, though growth rates slightly lagged those of January 2024. Based on data from Office of National Statistics (ONS) and major news sources.

Sector Performance Comparison

Independent Clothing Stores

Independent clothing stores continued their decline in January 2025, from the numbers published from ONS, sales decreased by 18.6% from December though less sharply than in Janurary 2024 where it decreased by 31.5%. Competition from online retailers, changing consumer preferences, and economic pressures on discretionary spending remain key challenges. The high street has been particularly affected, with several long-standing stores closing. Dinghams Cookshop in Salisbury shut after 40 years, citing unsustainable costs, while Dobbies closed its Northampton branch due to inflationary pressures. TimePiece, a family-run watch repair shop in Bolton, also shut after 19 years, reflecting declining foot traffic and the shift to online shopping. These closures highlight the persistent struggles faced by independent retailers.

Independent Household Goods Stores

January 2025 marked a positive shift for independent household goods retailers, from the numbers published from ONS, sales decreased by 0.6% with performance improving compared to January 2024 where it decreased by 6.5%. This resurgence can be linked to increased consumer investment in home improvements and furnishings, driven by a desire to enhance living spaces. The Construction Products Association forecasted 3% growth in private housing repair and improvement in 2025, reflecting a wider trend of spending in this area.

Additionally, Barclays reported a 6.3% rise in spending on ‘Insperiences’—at-home experiences—suggesting that consumers are prioritising home-related purchases. Promotional activities such as seasonal discounts, in-store exclusive deals, and bundle offers likely played a key role in attracting customers back to physical stores. Retailers may have also leveraged loyalty programmes, click-and-collect incentives, and interest-free credit options to encourage spending.

Independent Food Stores

After a robust performance in 2024, from the numbers published from ONS, sales for independent food stores experienced a downturn in January 2025 where there was a decrease of 2.8% while in 2024 there was an increase of 5.3%. This decline could be due to increased competition from larger supermarket chains, changes in consumer spending priorities post-holiday season, and potential supply chain disruptions affecting product availability.

Despite this short-term dip, the long-term outlook for these stores remains positive, supported by sustained consumer interest in locally sourced and specialty food products. NielsenIQ highlights that consumers continue to prioritize fresh, locally sourced, and organic foods, driven by health and environmental considerations. This trend underscores the resilience of independent food retailers catering to the growing demand for sustainable and high-quality food options.

Sports Equipment, Games, and Toys

The sports equipment, games, and toys sector experienced substantial growth in January 2025, from the numbers published from ONS, sales increased by 14.4%, building on an already successful 2024 where sales increased by 4.6%. This rise can be attributed to a growing consumer focus on health and fitness, with more people investing in home gym equipment, outdoor sports gear, and wellness-related products. A survey by PA Consulting found that four in five consumers planned new wellness and fitness purchases by 2025, reflecting a broader shift towards active lifestyles.

Additionally, the continued popularity of gaming and home entertainment contributed to strong sales in this category, as consumers sought high-quality leisure options. Experian reported that the UK’s health and wellness boom has driven increased spending in related markets, further supporting demand. Marketing campaigns promoting the latest sports technology and gaming innovations have also played a role in driving consumer engagement, making this one of the strongest-performing retail sectors in early 2025.

Computers and Telecom Equipment

In January 2025, the computers and telecom equipment sector continued to perform well from the numbers published from ONS, sales increased by 7.8%, driven by remote work trends and the need for up-to-date technology. However, growth rates were slightly lower than in January 2024 where there was an increase by 28.5%, likely due to market saturation and extended product lifecycles. As noted by the Corporate Finance Institute, market saturation leads to increased competition, shifting the focus from customer acquisition to retention.

Rapid technological advancements and shorter product lifecycles, as explained by Wharton, contribute to slower growth despite ongoing demand. According to S&P Global, the networking industry is also expected to experience moderate recovery in 2025 after a decline in 2024.

Retail Closures & Openings

The retail sector faced notable challenges, with several independent and long-standing stores closing due to economic pressures and shifting consumer behaviours. In 2024, the UK experienced a significant number of retail store closures. According to data from the Centre for Retail Research, a total of 13,479 shops closed during the year, averaging approximately 37 closures per day. Independent retailers were particularly affected, with 11,341 closures.

For instance, Hughes Electrical, a family-owned retailer, closed its Felixstowe branch after 40 years, citing the rise of online shopping as a significant factor.

The closure of Clitheroe Books, driven by rising property rents, highlights a broader issue affecting small businesses in town centres. Owner Paul Hamer expressed concern over the increasing number of non-retail establishments, such as barbers and vape shops, which he believes contribute to the “dumbing down” of the area. He pointed out that such businesses may not attract visitors in the same way a bookshop can, ultimately harming the town’s appeal. Hamer’s decision underscores the challenges small businesses face considering high rental costs and shifting local retail landscapes.

Similarly, The Original Factory Shop announced the closure of its Great Harwood store, influenced by lease terminations and broader high street struggles. These closures reflect the broader trend of declining physical retail presence, influenced by increased operational costs and the growing preference for online shopping.

Tee Tea, a bubble tea and dessert store in Brighton, was forced to close after its lease expired. Despite efforts from new owners to save the financially struggling business, the landlords requested the property back in February 2025. The café is now seeking public support via a GoFundMe campaign to help secure a new location and cover operational costs. The business plans to offer special discounts and free drinks to donors once they reopen in a new spot.

The retail sector is facing significant challenges, with several long-standing stores closing due to rising costs and changing consumer habits. Notable closures include Hughes Electrical in Felixstowe, Clitheroe Books, and The Original Factory Shop, each affected by factors like high rents, competition from online shopping, and shifting local retail dynamics. On the other hand, some businesses, such as Tee Tea in Brighton, are striving to reopen by seeking public support, reflecting the resilience of small retailers navigating economic pressures.

Consumer Trends & Behavioural Shifts

In January 2025, UK consumers exhibited a cautious yet adaptive spending approach, balancing online and in-store shopping preferences. According to Barclays Corporate Banking, overall retail spending increased by 1.2% year-on-year, with non-essential spending rising by 2.7%, driven by sectors like entertainment and health & beauty. However, the Confederation of British Industry reported that consumer-facing services firms experienced a significant decline in profitability, reflecting a cautious spending mindset among households.

Additionally, NielsenIQ noted a five-point drop in the UK Consumer Confidence Index to -22 in January, indicating prevailing economic uncertainties influencing more selective spending, particularly in categories such as clothing and food. Despite these challenges, certain sectors, notably health and beauty, have successfully attracted consumers back to physical stores, offering unique products and in-store experiences that resonate with the health and wellness trend.

Key Takeaways & Outlook

The UK retail sector in January 2025 demonstrates resilience amidst economic challenges. Sectors that have adapted to changing consumer preferences. This growth was particularly evident in health and beauty products, where spending rose by 10.7% according to the British Retail Consortium (BRC), influenced by social media trends and endorsements have seen positive outcomes.

However, traditional retail models, especially independent stores, must innovate and differentiate to remain competitive. Looking ahead, retailers should focus on enhancing digital presence and discoverability, offering unique in-store experiences, and closely monitoring consumer trends to navigate the evolving market landscape.

At Localverse, we help retailers stay ahead by providing data driven insights into shifting consumer trends, market demands, and competitive positioning. Our innovative products empower businesses to enhance their digital presence, optimise in store experiences, and adapt to changing retail dynamics with confidence. By leveraging our expertise, independent retailers can make informed decisions that drive growth and resilience in an evolving market. Contact Localverse today to discover how we can support your business.

Conclusion

In summary, January 2025 presented a mixed landscape for UK retailers. While certain sectors like household goods and sports equipment experienced growth, others, including independent clothing and food stores, faced challenges. The ongoing shift towards online shopping, coupled with economic pressures, underscores the need for retailers to adapt strategies that align with changing consumer behaviours and market dynamics.

The retail landscape is constantly evolving, shaped by shifting consumer behaviour, economic trends, and industry innovations. This analysis explores key insights behind the rise and fall of sales across various retail sectors in the UK from 2023 to 2024, based on data from the Office of National Statistics and major news sources.

Independent Clothing Stores

Independent clothing retailers in the UK faced significant struggles in 2024, with a widespread decline in sales compared to 2023

While there was some improvement during the holiday season, overall figures remained well below previous levels. The rising cost of living, high inflation, and increased operational expenses, including soaring energy costs and staff wages, placed substantial pressure on these businesses. Furthermore, the continued shift to online shopping made competition fierce, with many independent stores failing to maintain their customer base.

Independent Household Stores

Independent household goods stores also experienced sharp declines, failing to meet any of their 2023 quarterly sales figures. Major retailers such as DFS and Wickes reported weakened demand for high-cost household items, attributing this to consumers exercising caution with discretionary spending amid economic uncertainty. Rising mortgage rates and the broader cost-of-living crisis further dampened consumer confidence in making large purchases, significantly affecting the home improvement and furniture sectors.

Retail Store Closures

Store closures surged across the UK in 2024, with nearly 13,500 retail locations shutting their doors—marking a 28% increase from 2023. Independent retailers bore the brunt of this downturn, accounting for 84.1% of closures. Even established brands like Superdry and Ted Baker struggled, citing tough trading conditions and significant drops in revenue that led to the closure of multiple locations. The shift towards online retail, coupled with higher rent and business rates, contributed to the widespread downturn for brick-and-mortar stores.

Independent Food Stores

Conversely, independent food stores witnessed growth, driven by a record £1B in investments in 2024, up from £646M in 2023 This funding was directed toward store refurbishments, implementation of energy-efficient technologies, and crime prevention measures.

Consumer behaviour also played a role, as shoppers increasingly sought high-quality, locally sourced products. Upmarket grocers such as Booths saw a 6.7% rise in annual sales, exceeding £300M for the first time, as foot traffic and basket spend increased.

Castore & Telecom Sales

Castore, the British sportswear brand, reported a record-breaking trading period in December 2024, with a 16% rise in sales. The growth was fuelled by a surge in demand for football shirts and Formula One merchandise, reflecting the increasing influence of sports fandom on retail trends. The global sports and outdoor toys market is also on track to expand at a compound annual growth rate of 4.6% from 2025 to 2034, driven by heightened health consciousness and a shift towards active lifestyles and outdoor recreation.

The UK’s telecom and computer sectors saw significant gains in 2024, propelled by technological advancements and increased consumer spending. The release of new AI-driven products, particularly from major companies like Apple, led to a nearly 35% surge in sales of telecoms and computers in September alone. This contributed to a 1.9% overall increase in retail sales for the third quarter, the highest since mid-2021. Additionally, the UK telecommunications market grew to £22.12B in 2023, with forecasts indicating a compound annual growth rate of 5.1% from 2024 to 2032. This expansion is largely driven by the rapid deployment of 5G networks and the increasing adoption of Open RAN technology, which offers more flexible and cost-effective network solutions.

Conclusion

The UK retail sector in 2024 saw mixed fortunes, with some industries thriving while others struggled. Independent clothing and household goods stores faced declines due to rising costs and cautious spending, while sectors like food retail, fuel stations, and tech-driven markets benefited from strategic investments and shifting consumer preferences. Trends such as the rise of collectibles, health-focused spending, and AI advancements highlight the importance of adaptability. As the retail landscape continues to evolve, businesses that embrace innovation and respond to consumer needs will be best positioned for long-term success.